In today’s fast-paced world, financial planning has become a crucial aspect of our lives. Whether it’s saving for retirement, managing regular expenses, or fulfilling long-term financial needs, investors are constantly seeking efficient strategies to make the most of their investments. Moreover, due to the increasing rate of inflation, a second source of income or supplementary cash inflow may no longer be a luxury but a necessity.

If investors want regular cash flow from their investments the automatic choice for many, are bank fixed deposits, postal deposits, or rental income generated through real estate.

Mutual funds have a solution for this, called SWP (Systematic Withdrawal Plan).So, what is SWP in mutual fund?

Many of us are familiar with the concept of SIP (Systematic Investment Plan), which involves investing a fixed amount of money at regular intervals to build long-term wealth. In contrast to SIP, there is another investment strategy called SWP, where investors systematically withdraw a fixed amount from a scheme instead of investing money at regular intervals. SWP or Systematic Withdrawal Plan is a mutual fund investment plan, through which investors can withdraw fixed amounts at regular intervals, for example – monthly/ quarterly/ yearly from the investment they have made in any mutual fund scheme, at the same time they can generate a corpus at end maturity of scheme.

What are the Benefits of SWP?

– Post-retirement benefit: It acts as great source of regular income for retirees who lacks pension or other regular income, with which they can manage spending and financials needs post-retirement.

– Additional source of income: It also acts excellent source of income along job salary or business profits, they can receive equalised instalments at regular intervals as per their requirements, this can be for household expenses, retired parent’s support income, kid’s school fee or so on.

– Flexibility: Investor can customize the cash flows as desired; he can withdraw either a fixed amount or just the capital gains on his investments. SWP provides the investor with a regular income and returns on the money that is still invested in the scheme.

– Financial goal planning: On planning SWP acts as a great investment tool to meets once financial goals, which can be delayed due to non-availability of cash/cash crunch, is redemption is set when need of money is most.

How does it work?

Investor has to select mutual fund scheme according to the following factors:- age, funds appropriation in various risk classes i.e., Equity, Hybrid, Debt, period of scheme, frequency and amount of withdrawal at each interval according to respective needs and goals to be achieved

At each interval the mutual funds units will be withdrawn at respective NAV. With time, due to capital appreciation, the NAV will increase and the number of units to be withdrawn reduces to generate cashflows to serve each interval.

This helps investor to get cashflow at regular interval and generate corpus at maturity, to fit once need and plan as per requirement. This cycle can continue until investment value becomes 0 or scheme is cancelled.

Let us see a real life use case of this option.

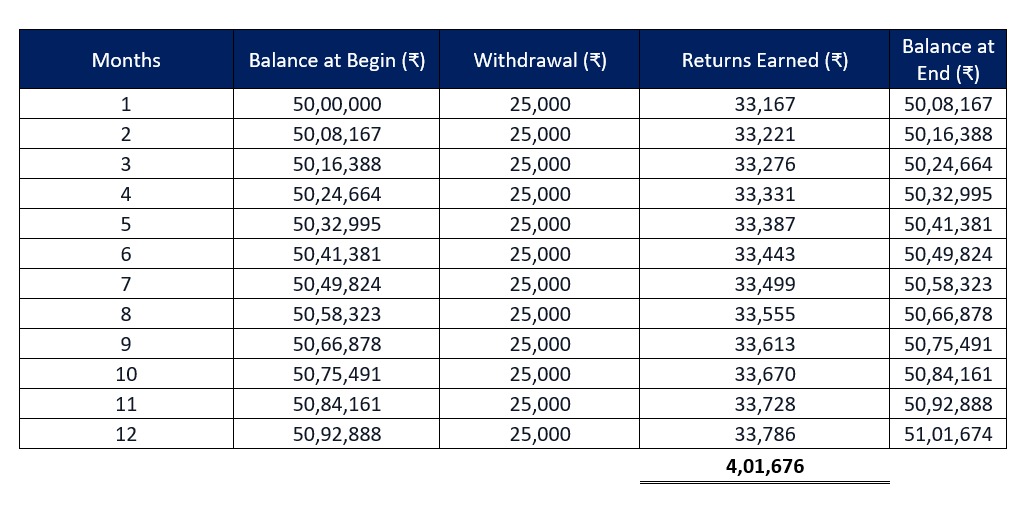

Mr. John who is about to retire in a few months has a corpus of ₹50 lacs with him. He decides to employ SWP strategy for his post retirement life income. Mr. John understood that he needed approx. ₹20,000-₹25,000 every month for his sustenance. Considering these circumstances, let us see how the entire calculation in this strategy would work:

Total one time Investment Amount= ₹50,00,000

Expected Return rate on the portfolio=8% p.a.

Monthly withdrawal amount=₹25,000

Annual withdrawal rate=6% p.a.

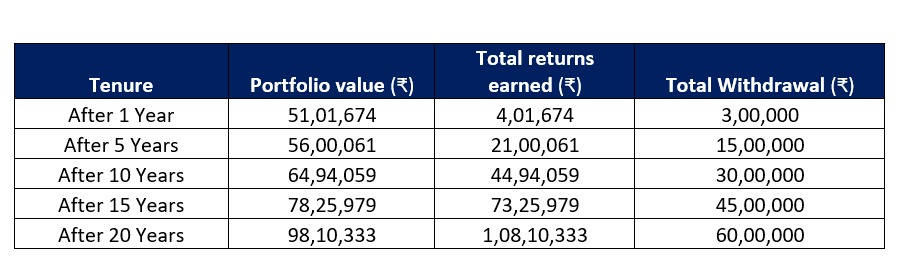

As evident from the above, though Mr. John was withdrawing a fixed amount on a monthly basis from his corpus, the corpus at the end of 20th year was still above the invested value. This is because of one single logic. i.e. the rate of withdrawal (as a percentage of portfolio value) is less than the rate of return earned by the portfolio. Hence, even though there is continuous withdrawal, the portfolio keeps on earning net returns, which keeps on increasing the corpus value.

In this same example, if Mr. John had withdrawn ₹40,000 per month, then the portfolio value at the end of 20th year would be ₹9,16,125. Thus, his corpus would have reduced as compared to initial investment. This is because of a simple reason that the annual withdrawal rate (9.60% in this example) is higher than the annual rate of return earned by the portfolio.

Thus, based on one’s needs, circumstances, and preference, the entire SWP strategy can be planned.

Thus, as clearly visible from the above example, retirees and senior citizens among the most common investors in this scheme. But that doesn’t mean younger people have nothing to learn from this. A person in his 20’s, 30’s or 40’s can plan to create a retirement corpus in future, using which he or she can do SWP. Thus, an individual can create a plan of SIP + SWP to secure his retirement in his younger working days itself.

How do you decide allocation of funds?

As SWP acts as tailored fit funds for people. There is no ideal allocation and it solely depends on income needs, corpus size, withdrawal frequency and instalments. Also, crucial decision is appropriate mix on funds in debt, equity, and hybrid funds which allows one to cater to regular withdrawing and building corpus at same time as annual drawings are funded from return which corpus funds.

The allocation of funds in initial years would be higher on equity size as they would result enormous growth in corpus at same time drawing would be lower, which in later years would give higher regular drawings and margin of safety to upheld any market downswing.

For example, the corpus size is 1 crore and annual drawing are 6 lakhs i.e. 6% of amount invested, funds earn return 12% the corpus at year end post withdrawal would stand at 1.06 crore which at next year would build more capital for generating return, vice versa.

In scenario where corpus size is restricted and higher regular funds for daily expense are required no option is left but to invest in debt instruments and conservative hybrid funds, where an assured return is required to fund regular payments, and margin of safety is lower to withstand bearish market in cases where withdrawal rate are higher than returns, would result in capital erosion.

What are its Tax implications:

Systematic Withdrawal Plans (SWP) are great form of investment in terms of tax efficiency as they serve routine cashflows at lower tax rate impacting cashflows as compared to other investments such as real estate rental yields/ interest on deposits.

SWP lets you strategically plan your withdrawals to optimize your tax liability, ensuring you make the most of tax-efficient investment options.

The rental yield and interest, which is taxed on respective slab rates of individual, the long-term gains are taxed at comparatively lower rates along with benefit of indexation.

Thus, tax applicability can be summarized as follows:-

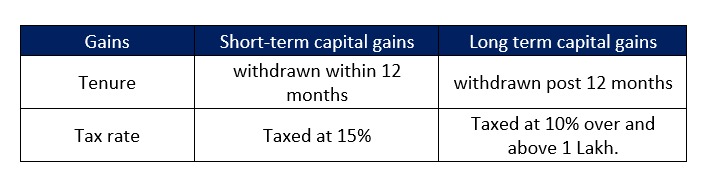

Equity-oriented mutual funds

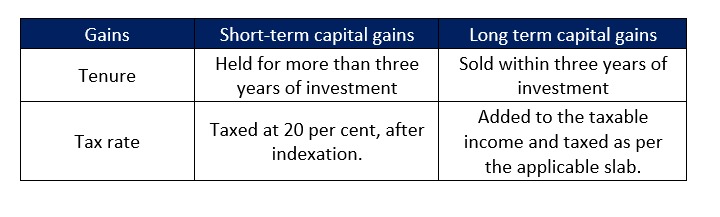

Non-equity oriented mutual funds

Conclusion:

A systematic withdrawal plan (SWP) is mutual fund scheme which helps you attain financial objectives with regular cashflow at specifies tenure along with corpus at maturity, which is more flexible and tax beneficial as compared to other instruments i.e. bank interest, pension/annuity schemes which can be used by retirees, non-regular income earners, goal oriented or risk averse investor to achieve objective or create an emergency or fund secured from market volatility. Incorporating SWP scheme in your portfolio would be a step ahead towards financial independence with planned/systematic approach, and enjoy a financially stable life.

We at RichVik Wealth, encourage as well as assist our clients to incorporate the SWP strategy in their financial planning.

To understand more on the topic as well as to start investments please feel free to contact us:

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is co-authored by Mr. Sahil Chichiria and Mr. Mayur Solanki from Team RichVik