As we all know that currently Equity markets are at an all-time high. In such a scenario, there can be a situation of volatility and investors can seek for some other options for weathering this volatility. Having a fixed income portfolio within your asset allocation that can weather such storms is crucial for preserving capital and achieving long-term financial goals. This article explores strategies to construct a resilient fixed income portfolio in the face of market turbulence.

Traditionally, FD, Government bonds, Debentures, & money market instruments formed major portion of the Fixed Income investment avenues available. However, now there are a lot of new age financial products upcoming which one can incorporate in one’s asset allocation towards Fixed Income. The yield on these products can be as low as 8% to as high as 20%.

The investors can bifurcate their Fixed Income portfolio in to two parts:

– Core portfolio: Traditional Fixed Income products

– Opportunity portfolio: New age Fixed Income products

Some of the widely known traditional Fixed Income instruments are as follows:

– Bank Fixed Deposits

– Government Bonds

– Debentures

– Public Provident Fund

– National Savings Certificates

– Debt Mutual Funds

Now, let’s see what are the new age Fixed Income alternatives available:

– P2P Lending (Peer to Peer Lending)

It is investment that allows people to lend or borrow money from one another without going to bank. P2P is the lending Platform that connects borrowers with Individual lenders directly through websites. Investors can earn returns by lending money to borrower receiving interest payments.

Within P2P space, there can two types of models:

a) Where investor selects the borrower and Platform acts as an intermediary.

b) Where investor deposits money with the Platform and funds are allocated to borrowers by the Platform.

Example for the both the cases:

a) Rahul as investor registers himself on a P2P lending platform say XYZ Company. He deposits 10,000. Arjun a small business owner applies for a loan on XYZ Company. He fills out a detailed financial profile which will be checked by the platform.

Based on Arjun’s financial profile and creditworthiness, XYZ Company assigns him a risk category. This risk category determines the interest rate Arjun will have to pay.

Rahul reviews various loan applications on XYZ Company and decides to fund Arjun loan request because he is comfortable with the risk category and the return (interest rate). The platform facilitates the loan agreement between Rahul and Arjun.

Arjun then makes monthly repayments (principal + interest) through the platform, which are credited back to Rahul’s account.

b) Rahul as investor registers himself on a P2P lending platform say XYZ Company. He deposits 10,000. Based on the tenure of deposit of the Rahul, XYZ Company allocates the funds of Rahul towards different borrowers with different loan maturities.

Opportunities & Risks in P2P Lending

– Fractional Real Estate

This Investment Structure allows you to buy a piece or the portion of the real estate property. There is no need to buy an entire property. In simple words, investors get a way to own an share of high value property at a low cost instead of buying the entire property at the higher cost.

For an Example

Let’s say there’s a building worth Rs 1 crore. This is quite expensive for one person to buy. But what if 100 people come together and each person contributes ₹1 lakhs? Now, each person owns 1% of the building. Now, all the investors can earn rental yield from the property.

Opportunities & Risks in Fractional Real Estate

– Asset Leasing

Leasing is an agreement between a lender, the lessor and a borrower, the lessee. The owner of the asset an individual or a company leases the asset to the borrower for a specific period and at a certain cost. The lessee is provided use of the asset in exchange for periodic payments throughout the agreed-upon lease term. Assets leased may include machinery, equipment, or vehicles.

For an Example

A company might be in need of a machinery. Multiple investors come together and invest their funds against specific assets required by the company. The investor holds ownership of these assets for a fixed tenure post, after which they get a promised sum. During this tenure, the investor receives a fixed payout, which includes interest and part of their investment.

Opportunities & Risks in Asset leasing

– Senior Secured Bond

These bonds are a type of debt security that takes more priority over other debts in the event of a company’s default. These bonds are backed by collateral such as property, which can be used to recover money in case of default.

Here’s how they work:

– Issuance: Typically, large corporations or Non-Banking Financial Companies (NBFCs) issue these bonds to raise funds from the market.

– Investment: Investors purchase these bonds, providing the issuer with the capital they need. The issuer promises to pay the investors a fixed rate of interest over a specified period.

– Collateral: The bonds are secured by specific assets of the company. If the company defaults these assets can be sold to repay the bondholders.

– Seniority: In the event of a default, Senior Secured Bondholders are the first to be repaid, even before other unsecured or subordinated debt holders.

– Maturity: At the end of the bond’s term, the issuer repays the principal amount to the bondholders.

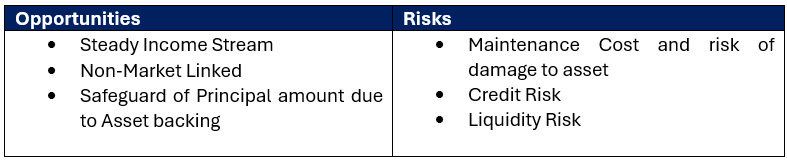

Opportunities & Risks in Senior Secured Bond

Conclusion:

Exploring alternatives to traditional fixed income investments can offer investors opportunity for greater flexibility, diversification, & potentially higher returns. While traditional products remain a stable choice for investors, alternative option can help individuals maximize their return & adopt evolving market conditions.

We at RichVik Wealth, help our clients diversify their Fixed Income Portfolio and take advantage of the new age products along with the stability provided by the traditional products.

To understand more on the topic as well as to start investments please feel free to contact us:

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is authored by Mr. Saurabh Gosavi from Team RichVik