A Fixed deposit is a financial instrument offered by banks, post office, and other NBFCs (Non-Banking Financial Company) which offers the investors a higher rate of interest compared to regular savings or a salary account. Typical investors in fixed deposits are the ones who would have already accumulated surplus cash over a period of time. For this reason, fixed deposits are a popular choice of investments for retired individuals and senior citizens.

FD rates across major banks (7 days to 10 years)

| Banks | Interest Rates on FD’s |

| SBI | 3.00% – 6.50% |

| HDFC | 3.00% – 7.00% |

| ICICI | 3.00% – 6.90% |

| Axis | 3.50% – 7.00% |

| Canara Bank | 4.00% – 6.70% |

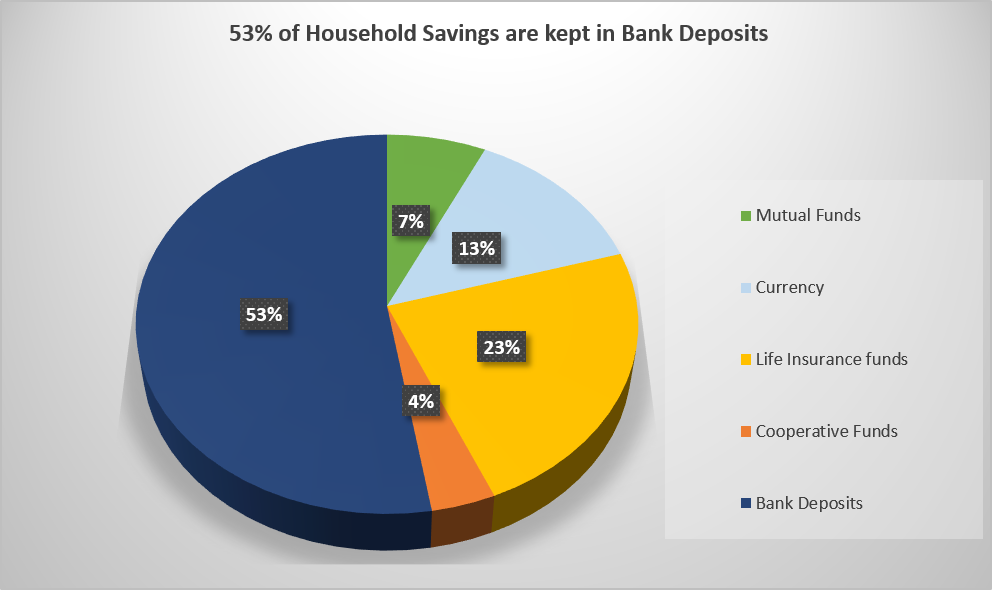

What has happened actually is that we have all been reliant on Fixed Deposits as a place we park our money and we get steady returns and trend has been persistent since 1980’s. As we can witness from the above, it has been about 50-60% range our allocation to Bank deposits which has been predominant as compared to others. However, there is uncertainty with respect to whether Fixed Deposits can beat the inflation rate consistently. Hence, to beat the inflation rate, investors need to look beyond Fixed Deposits.

So, Equities or Fixed Income? How do you pick the winning asset class?

It is a challenge to consistently pick winners amidst unpredictability and volatility

There have been years when equity markets had a brilliant run, years when only bonds were dependable, and these periods did not typically overlap.

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

| Sensex | 49% | 49% | -52% | 83% | 19% | -24% | 28% | 11% | 32% | -4% | 3% | 30% | 7% | 14% | 17% |

| Bonds | 4% | 7% | 9% | 4% | 5% | 7% | 9% | 4% | 14% | 9% | 13% | 13% | 6% | 11% | 12% |

Imagine someone holding on all equity portfolio in 2008, or holding none in the equity rally that followed?

Hence, investors need to combine asset classes for better Risk adjusted returns, so that one’s asset down cycle is balanced by another asset’s up cycle, where each asset serves a role in a portfolio context.

Equity- Provides Long term growth

Fixed Income- Regular Income and stability

But what is the right balance of equity and debt?

Thankfully, this is the exact question addressed by

Dynamic asset allocation funds.

As the name suggests, these funds:-

– Dynamically allocate money between equity and debt based on a pre-set model that assesses and analyses market conditions.

– When the market offers favourable equity valuations (which can provide good returns for the investor) the fund dynamically invests more in equities.

– When equity valuations are expensive, the fund reduces equity allocation and increases its capital allocation to debt or arbitrage.

Also, from tax point of view, Mutual Funds are classified as equity funds when there is equity exposure of at least 65%. When you redeem your equity fund units within a holding period of one year, you will realize short-term capital gains. Regardless of your income tax bracket, these gains are taxed at a flat rate of 15%, otherwise Long term capital gain tax will be applicable at 10%, in excess of 1 lacs without indexation benefit.

| Return Comparability between FD’s and Dynamic Funds | ||

| Fixed Deposit | Dynamic Asset allocation funds | |

| Invested Amount | 20,00,000 | 20,00,000 |

| No. of Years Invested | 3 Years | 3 Years |

| Annual Interest /Return (%) | 6.40% | 9.91% (Category average of 3 years) |

| Redeemed Amount | 24,09,100 | 26,55,471 |

| Profit Before Tax | 4,09,100 | 6,55,471 |

| Calculation of Profit after Tax | ||

| Tax | 1,27,639 | 55,547 |

| Profit after Tax | 2,81,461 | 5,99,924 |

Dynamic asset allocation funds make these allocations based on fundamental valuation indicators such as price/earnings ratios, price/book value and technical indicators such as historical moving averages.

However, the fundamental problem of Hybrid category mutual funds is that a Portfolio with 65% equity exposure would wipe out 40% of the capital if the markets fall by 60%, which would be sufficient to keep Indian households and Investors at bay from investing via mutual funds.

So, to achieve a reasonable return but with significantly low drawdowns so that people can have & use their money when they really want to, introducing- Samco Dynamic Asset Allocation Fund. It is built on the Transformer model, and works on the principle –Trend is your friend i.e., sometimes there’s no need to have debt exposure at all, when the fund holds equity allocation in uptrends, and completely transforms to a debt + arbitrage mode with no equity in bear markets to minimize downside.

Salient features of SAMCO Dynamic Asset Allocation Fund:-

– Allocations are made between equity, debt /cash based on market trends.

– Model Driven- Rebalancing decisions are based on a well-defined and time-tested model that removes biases of any kind.

– Tax Efficiency- Allocation across different asset classes gives investors the benefit of equity taxation.

– Fund for all markets- Risk adjusted returns are similar to investments in equity and with low volatility across market conditions.

SAMCO Dynamic Asset Allocation fund can be compared to transformer model that is designed to switch between equity to debt and vice versa based on market trends with an aim to provide consistent returns and simultaneously protect drawdowns. Imagine a car is cruising along the highway, and the vehicle ahead loses control, causing it to skid, but the car transforms to a humanoid bot, avoiding the accident and again transforming to a vehicle to continue cruising on the highway.

This metaphor parallels the capability of Dynamic asset allocation fund, which adjusts its allocation between debt and equity in response to prevailing market conditions.

Conclusion: -The choice between Dynamic Funds and Fixed deposits depends on an individual’s risk tolerance, investment horizon, and financial goals. Fixed deposits offer the fixed returns and are suitable for investors seeking low-risk options. Dynamic funds have the potential to generate higher returns but also carry slightly higher risk. Investors with moderate risk appetite and investment horizon of 3-5 years may find Dynamic funds more attractive.

To avail the opportunity of investing in such a Dynamic Fund, you can invest in the Dynamic Asset Allocation Fund of SAMCO, NFO of which opens from 07/12/23 till 21/12/23.

To understand more on the topic as well as to start investments please feel free to contact us:

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is authored by Mr. Mayur Solanki from Team RichVik.