In the previous blog about the National Pension System (NPS), we have covered as to how it can be used as a retirement tool. However, it is not just a tool for retirement but also a tax-saving tool too. Think of it as a two-for-one deal that not only does help you secure money for the golden years, but it also slashes your tax outflow in the process. By investing in NPS, you can trim down your taxable income, thanks to deductions under Sections 80C and 80CCD (1B) of the Income Tax Act.

A pension secures financial stability during retirement, providing a reliable source of income. It empowers individuals to embrace retirement with dignity and freedom from financial worries. Considering that most people today either are working in Private sector or are self-employed, the idea of NPS becomes even more important. This scheme encourages people to invest in a pension account at regular intervals during the course of their employment. After retirement, the subscribers can take out a certain percentage of the corpus. As an NPS account holder, you will receive the remaining amount as a monthly pension post your retirement.

Thus, NPS is ideal for self-employed professionals like lawyers, doctors, chartered accountants, entrepreneurs, architects, journalists, chefs, freelancers wherein no employer is attached, or even for those in the private sector. The NPS stands out as a reliable option for the private sector workforce providing a safety net for their golden years.

Moreover, NPS offers a modern approach to retirement planning, allowing you to diversify your investments across various assets and grow your nest egg systematically. Therefore, whether you are dreaming of early retirement or simply want to secure your financial future, NPS has your back, making tax saving and retirement planning a breeze in today’s fast-paced world.

So, let us take a quick recap about National Pension Scheme:

The National Pension Scheme (NPS) is a Central Government scheme in which any individual citizen (either salaried or non-salaried) of India (both resident and non-resident) between the ages of 18 and 70 can participate and set aside an amount on a regular basis.

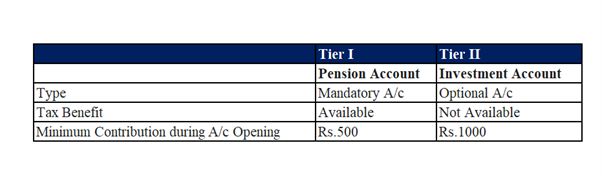

What type of accounts NPS offers to its subscribers?

Tier I:

The primary account, which is a pension account, which has restrictions on withdrawals and utilization of accumulated corpus. All the tax breaks that NPS offers are applicable only to Tier I account.

Tier II:

In order to introduce some liquidity to the scheme, the PFRDA allows for a Tier II account where subscribers with pre-existing Tier I accounts can deposit and withdraw money as and when they want. Tier II is an investment account, similar to a mutual fund in characteristics, but offers no exit load, no commissions, and good returns.

Exit Option under Tier I:

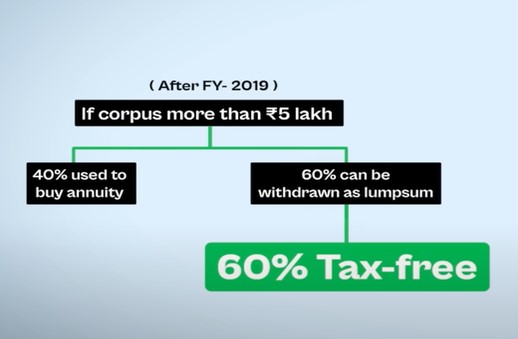

On attaining age of 60 years:

– If total corpus is equal or less than Rs.5.00 Lacs, then entire corpus can be withdrawn.

– If total corpus is more than Rs.5.00 Lacs then, Minimum 40% of the corpus needs to be invested in Annuity Scheme (Taxable as per Slab) and 60% of the corpus can be commuted/withdrawn in lump sum/ staggered anytime up to age of 75 years (Tax free).

Before 60 years of age (after completion of 5 years):

– 20% of the corpus can be withdrawn in lump sum

– 80% of the corpus will be invested in a ‘Annuity Scheme’

– If total corpus is equal or less than Rs.2.50 Lacs, then entire corpus can be withdrawn.

Withdrawal Option under Tier I:

Part Withdrawals under Tier I

– A partial withdrawal of accumulated pension wealth, not exceeding 25% of the employee contributions, after a lock in period of 3 years.

– Allowed to withdraw only a maximum of three (3) times during the entire tenure subject to conditions prescribed by the Regulator.

Tax benefits: Applicable for investments in Tier I account

Tax Benefit available to Individual:

Any individual who is Subscriber of NPS can claim tax benefit under Sec 80 CCD (1) within the overall ceiling of Rs.1.5 lacs

An additional deduction for investment up to Rs.50,000 in NPS (Tier I account) is available exclusively to NPS subscribers under subsection 80CCD (1B). This is over and above the deduction of Rs.1.5 lakh available under section 80C of Income Tax Act. 1961.

Tax Benefit available to Corporates:

Additional Tax Benefit is available to Subscribers under Corporate Sector, u/s 80CCD (2) of Income Tax Act.

Employer’s NPS contribution (for the benefit of employee) up to 10% of salary (Basic + DA), is deductible from taxable income, up-to 7.5 Lakh.

Let us understand from below example, how Withdrawal/Exit Option will work along with its taxability:-

Example 1: Part Withdrawals under Tier I

Meet Riya: A 45-year-old teacher with an NPS corpus of Rs.7 lakhs. Unfortunately, her son requires urgent medical treatment, estimated to cost Rs.5 lakhs.

– Withdrawal Option: Riya can opt for a partial withdrawal of 25% of her own contributions, excluding employer contributions (if any). In this case, she can withdraw 25% of Rs.7 lakhs, which is Rs.1.75 lakhs.

Tax Implications: Entire 25% Partial withdrawal i.e. 1.75 lakhs are tax-free.

Benefits-Riya can access immediate funds for her son’s treatment while retaining a significant portion of her retirement corpus.

Example 2: Exit Option on attaining age of 60 years:

Meet Rajeev: A 62-year-old businessperson with an NPS corpus of Rs.25 lakhs. He wishes to retire and enjoy a regular monthly income.

– Withdrawal Option: Rajeev can choose to utilize 40% of his corpus to purchase an annuity, securing a guaranteed monthly pension for life. The remaining 60% can be withdrawn as a lump sum.

Annuity purchase amount: 40% of Rs.25 lakhs = Rs.10 lakhs

Lump sum withdrawal: 60% of Rs.25 lakhs = Rs.15 lakhs

Tax Implications: The 40% used for annuity purchase is taxable as per Rajeev’s income slab. The Rs.15 lakhs lump sum withdrawal is tax-free.

Conclusion: – NPS empowers you to build your retirement plans along with Tax savings. So, take control of your golden years with a smart tax savvy decision. Open an NPS account today and watch your retirement dreams take flight.

We at RichVik Wealth, enable NPS investments for our clients to ensure their retirement investments are tax savvy.

To understand NPS in more detail, you can visit our previous blog on NPS at: https://richvikwealth.in/securing-your-future-a-deep-dive-into-the-national-pension-scheme-nps/

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is co-authored by Ms. Diksha Parab and Mr. Saurabh Gosavi from Team RichVik