In the realm of financial planning and wealth management, the Hindu Undivided Family (HUF) structure presents a unique avenue for investors to optimize their assets and minimize tax liabilities. This article explores the key aspects of HUFs from an investor’s standpoint, shedding light on the potential benefits and considerations associated with the HUF. The concept of a Hindu Undivided Family (HUF) as a separate entity for tax purposes was first recognized in 1917. Formed under Hindu law, the HUF is a legal entity that allows families to pool their resources and manage them collectively over the years.

Formation and Structure

Hindu Undivided Family (HUF) consists of individuals who have lineally descended from a common ancestor and are bound together by the ties of blood and affection. The head of the family, known as the ‘Karta’, manages the HUF’s affairs. The assets brought into the HUF can include ancestral properties, gifts, and income generated by the family members. You can lower your tax liability by creating a family unit and merging your assets into a HUF. Independent of its constituents, HUF is taxed. A collection of Hindu households can form a HUF and also HUF has its own PAN and submits tax returns separately from its members.

Investment Opportunities

– Shares and Mutual Funds

HUFs can invest in a wide range of financial instruments and assets, similar to individual investors. This includes stocks, mutual funds, real estate, fixed deposits, and more. The pooled resources of the HUF can lead to more substantial investments, potentially resulting in higher returns. Additionally, the HUF can benefit from the tax efficiency of certain investment instruments, contributing to overall wealth creation.

– House Property

An individual is only allowed to have a two self-occupied properties as per the Income Tax laws. In case if an individual owns more than two properties, then it will be considered as ‘deemed to be let out’. Tax should be paid as per the notional rent on such properties. However, HUFs are allowed to own residential properties. So, if a HUF member owns more than two properties, the deemed let property can be in the name of the HUF and thus optimize the tax outflows.

Tax Benefits and its implications on your wealth

As per the Income Tax Act, being a separate entity, the HUF enjoys a basic tax exemption of ₹ 2.5 lakh. One of the primary advantages of the HUF structure is its favorable tax treatment. HUFs enjoy their own tax exemptions and deductions, which can lead to significant tax savings. HUFs are also allowed to claim tax deductions on premiums paid for life insurance and health insurance. So, a HUF member can claim a tax deduction of up to ₹ 1.5 lakh on premiums paid for a life insurance policy. Similarly, there are tax deductions of up to ₹25,000 on premiums paid for a health insurance policy.

For example, an HUF can avail of tax exemptions under sections 80C, 80D, and other provisions of the Income Tax Act, providing additional avenues for wealth accumulation.

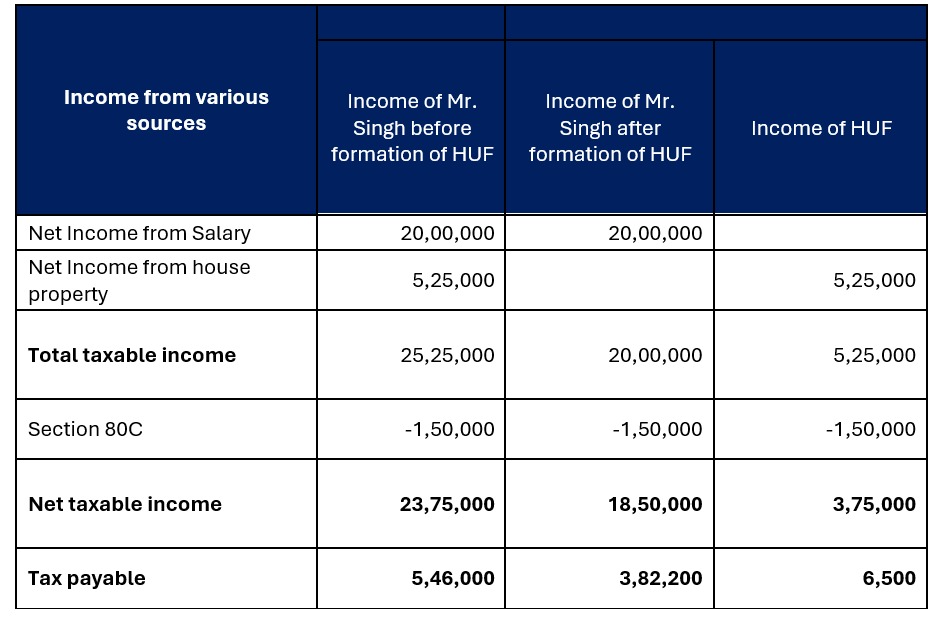

Let’s understand how an HUF is taxed with an example: –

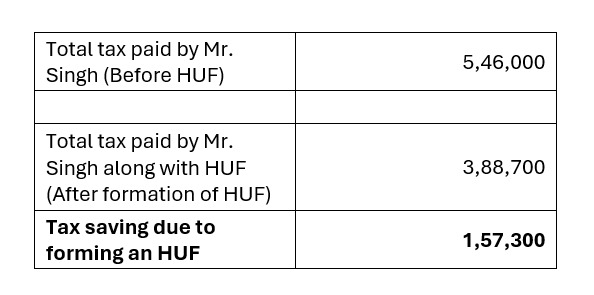

After the death of his father, Mr. Aman Singh decides to start a HUF with his wife, son, and daughter as members. Since Mr. Singh had no siblings, the property held by his father was easily transferred in the name of the HUF. The property held by late Mr. Singh earns an annual rent of ₹7.5 lakhs. Mr. Aman Singh has an income from salary of ₹20 lakh. By creating a HUF, Mr. Singh can save tax as below: –

So, consistent savings of around ₹1,57,300 invested at market growth of around 13%, can potentially lead to significant wealth accumulation, turning someone into a crorepati over the course of 20-25 years.

Succession Planning

The HUF structure facilitates smooth succession planning within a family. Assets within the HUF can be passed down through generations without the need for complex legal procedures. This can be particularly advantageous in preserving family wealth and ensuring a seamless transition of assets to the next generation.

Challenges

While the HUF offers various benefits, investors must also be aware of certain challenges. The concept of HUF is rooted in traditional Hindu law, and its applicability may vary for individuals from different religions. Furthermore, changes in tax laws and regulations may impact the benefits associated with the HUF structure. It is crucial for investors to stay informed and adapt their strategies accordingly.

Conclusion:

In conclusion, the Hindu Undivided Family provides investors with a powerful tool for wealth accumulation, tax optimization, and succession planning. Hence, investors can create a robust financial foundation that stands the test of time, aligning with their broader investment objectives and family legacy goals.

We at RichVik Wealth, strategically leveraging the benefits of HUFs, help our clients to optimize their taxes and create wealth.

To understand more on the topic as well as to start investments please feel free to contact us:

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is co-authored by Ms. Shraddha Pankar and Mr. Mayur Solanki from Team RichVik