Behavioural finance bridges the gap between psychology and economics by exploring how cognitive biases and emotions influence investor behaviour. Unlike traditional finance, which assumes rationality and efficiency, behavioural finance recognizes that real-world investors often act irrationally, leading to mispricing, bubbles, and crashes.

“Behavioural finance is the study of the influence of psychology on the behaviour of investors or financial analysts and the subsequent effect on markets.”— Martin Sewell (University of Cambridge 2007)

– Behavioral Finance vs. Traditional Finance

| Aspect | Traditional Finance | Behavioural Finance |

| Assumptions | Investors are rational and self-interested | Investors are often irrational and emotional |

| Market Behaviour | Markets are efficient | Markets are inefficient due to behavioural biases |

| Decision Making | Based on all available information | Influenced by biases, heuristics, and emotions |

| Risk Perception | Objective and quantifiable | Subjective and inconsistent |

| Investment Models | CAPM, EMH, Modern Portfolio Theory | Prospect Theory, Mental Accounting, etc. |

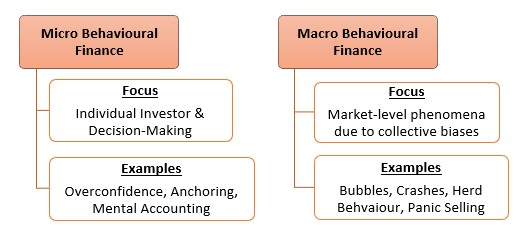

– Micro vs. Macro Behavioural Finance

– Common Biases and Their Impact on Investment Decisions

| Bias | Description | Impact on Investment Decisions |

| Overconfidence | Overestimating knowledge and predictive abilities | Excessive trading, underestimating risks |

| Anchoring | Relying too heavily on initial information | Poor valuation estimates, ignoring new data |

| Loss Aversion | Losses feel more painful than equivalent gains feel good | Holding onto losing assets too long, fearing to realize a loss |

| Herd Behaviour | Mimicking others’ decisions without independent analysis | Bubbles, market volatility |

| Confirmation Bias | Focusing on information that supports existing beliefs | Ignoring contrary evidence, reinforcing poor decisions |

| Mental Accounting | Treating money differently based on arbitrary categories | Suboptimal asset allocation, inconsistent risk tolerance |

– Other Notable Biases

Disposition Effect: Tendency to sell winners too early and hold onto losers.

Trend Chasing: Investing in assets simply because they have recently performed well, often buying high and selling low.

Limited Attention Span: Focusing only on investments that are in the media spotlight, rather than conducting thorough research.

Endowment Effect: Overvaluing assets simply because you own them.

Self-Attribution: Overestimating one’s own knowledge or skill in making investment decisions, ignoring expert advice.

– Investor Decision Flow (Simplified)

[Market News]

↓

[Emotional Reaction] → [Bias Activation: Loss Aversion, Herding, etc.]

↓

[Investment Decision: Buy, Sell, Hold]

| Emotional State | Typical Investor Behaviour | Market Outcome |

| Joy/Exuberance | Increased risk-taking, optimistic buying | Asset bubbles, rising prices, lower volatility |

| Fear/Anxiety | Panic selling, risk aversion, and impulsiveness | Sharp downturns, high volatility, price drops |

| Greed | Chasing gains, ignoring risks | Overvaluation, unsustainable rallies |

| Overconfidence | Excessive trading, underestimating risks | Increased turnover, potential mispricing |

| Calm/Neutral | Rational, steady decision-making | Stable prices, lower volatility |

| Regret | Hesitation in re-entering the market | Missed opportunities |

– Summary Table: Emotional States and Market Outcomes

Real-World Examples

Dot-com Bubble (1995–2000): Driven by herd behaviour and overconfidence, tech stocks were wildly overvalued before crashing.

2008 Global Financial Crisis: Anchoring and optimism bias led many to underestimate the risk of mortgage-backed securities.

GameStop Mania (2021): Herd behaviour via social media (Reddit’s r/WallStreetBets) caused massive volatility and irrational valuations.

COVID-19 Market Panic: Emotional gap and loss aversion triggered panic selling, followed by herd-driven rallies as markets recovered.

– How Behavioural Finance Influences Your Spending Habits

Behavioural finance doesn’t just affect big investment decisions – it plays a quiet but powerful role in everyday spending too. Here’s how:

You treat money differently based on where it comes from. A salary feels serious, but a cashback or gift often feels like “free money,” leading to impulsive spending.

Discounts and “deals” trick you into buying things you don’t need. Your brain focuses on the original price and thinks you’re saving even when you’re still overspending.

You tend to spend now and think later. The desire for instant gratification often wins over long-term goals, like saving or investing.

You keep spending on things just because you’ve already paid. Whether it’s a gym membership or an expensive item you rarely use, you hesitate to let go because of what’s already been spent.

You follow what others are buying. Online trends, social media influencers, or peer pressure push you toward spending just to keep up.

– Practical Implications for Investors

Portfolio Management: Recognising and mitigating personal biases can lead to more effective asset allocation and risk management.

Risk Perception: Understanding that emotions influence risk tolerance can help investors make more rational choices during market volatility.

Market Efficiency: Behavioural finance explains why markets may not always reflect true asset values, creating opportunities and risks for investors.

Awareness and Education: Learning about common biases to improve decision-making.

Set Investment Rules: Predefined strategies or checklists help reduce emotional and impulsive decisions.

Diversification: Reduces exposure to emotional swings in specific assets.

Avoid Market Noise: Stay focused on long-term goals rather than daily news.

Behavioural Coaching: A financial advisor or coach can offer guidance during emotionally challenging market phases.

Journaling Investments: Documenting your investment rationale can help identify and correct biased patterns.

Conclusion

Behavioural finance offers a more realistic lens through which we understand investor behaviour. Recognising and mitigating psychological biases can lead to better financial outcomes and more stable markets. As financial markets grow more complex, understanding human behaviour becomes just as critical as mastering numbers.

To understand more on the topic as well as to start investments please feel free to contact us:

Phone: +91-9324609115

E-mail: team@richvikwealth.in

The article is authored by Ms. Sapna Yadav from Team RichVik.