Financial planning is the process of setting and achieving specific financial goals by assessing an individual’s current financial situation, analyzing their future needs and aspirations, and developing strategies to meet those goals. It involves evaluating various aspects of personal finances, such as income, expenses, savings, investments, taxes, insurance, and retirement planning, to create a comprehensive plan for managing money effectively.

Here are some common financial planning mistakes that should be avoided:

1. Failing to set clear financial goals:

Without specific goals, it’s difficult to create an effective financial plan. Define your short-term and long-term goals, such as paying off debt, buying a house, or saving for retirement. Here are a few examples of individuals failing to set clear financial goals:

– Mr. A’s Overspending: Mr. A has a well-paying job, but he never set any financial goals for himself. As a result, he indulges in impulsive purchases and frequently spends beyond his means. He fails to save money or invest for the future, leading to financial instability and a lack of progress towards his long-term financial objectives.

– Mr. P’s Aimless Investing: Mr. P starts investing without setting clear financial goals or understanding his risk tolerance. He jumps into different investments based on tips from friends or the latest trends, without a strategy in mind. As a result, he lacks a diversified portfolio and exposes himself to unnecessary risks, potentially leading to significant losses.

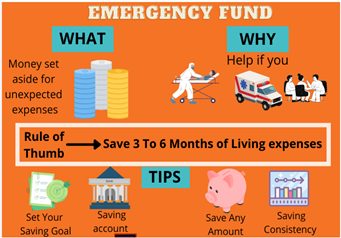

2. Neglecting an emergency fund:

It’s crucial to have an emergency fund to cover unexpected expenses. Aim to save three to six months’ worth of living expenses in a readily accessible account. Neglecting to establish and maintain an emergency fund can leave individuals vulnerable to financial hardships when unexpected expenses arise. Here are a few examples that illustrate the consequences of neglecting an emergency fund:

– Ms. B’s Unforeseen Medical Expenses: Ms. B did not prioritize building an emergency fund. Suddenly, she experiences a medical emergency that requires expensive treatments. Without an emergency fund, she is forced to rely on credit cards or loans to cover the medical bills, leading to a cycle of debt and financial strain.

– Mr. M’s Job Loss: Mr. M loses his job unexpectedly due to company downsizing. Since he neglected to save for emergencies, he is ill-prepared to handle the sudden loss of income. He struggles to meet his financial obligations, including rent, bills, and daily expenses, causing stress and potentially leading to missed payments and financial difficulties.

3. Not budgeting or tracking expenses:

Without a budget, it’s challenging to manage your finances effectively. Create a budget to track your income and expenses, and regularly review it to make necessary adjustments. Neglecting to budget or track expenses can lead to financial disorganization, overspending, and difficulty in achieving long-term financial goals. Here are a few examples that illustrate the consequences of not budgeting or tracking expenses:

– Ms. E’s Inability to Save: Ms. E doesn’t track her expenses or establish a budget, making it challenging for her to save money. She has no idea how much she spends on discretionary items versus essential expenses. Without a clear budget, Ms. E finds it difficult to cut unnecessary expenses and allocate money towards savings, hindering her ability to build an emergency fund or work towards her financial goals.

– Mr. J’s Inefficient Financial Management: Mr. J neglects to budget or track his expenses, resulting in inefficient financial management. He has multiple bank accounts, credit cards, and subscriptions, but he doesn’t keep track of their balances, fees, or due dates. As a result, he incurs unnecessary fees, misses payment deadlines, and fails to optimize his financial resources effectively.

4. Availing unnecessary high-interest debt:

High-interest debt, such as credit card balances, can quickly accumulate and hinder your financial progress. Prioritize paying off these debts to minimize interest charges. Carrying high-interest debt can be financially burdensome and hinder individuals from achieving their financial goals. Here is an example that illustrate the result of carrying high-interest debt:

– Mr. S’s Credit Card Debt: Mr. S regularly uses his credit cards to cover his expenses but fails to pay off the balance in full each month. As a result, he accumulates high-interest credit card debt. The high-interest rates make it challenging for Mr. S to make significant progress in paying off the debt, and he finds himself trapped in a cycle of minimum payments and accruing interest, prolonging his debt repayment journey.

5. Ignoring retirement planning:

Start saving for retirement as early as possible to take advantage of compounding growth. Contribute regularly to retirement accounts like PFs, PPFs or create an SWP plan for post-retirement benefit. Ignoring retirement planning can have significant consequences for individuals’ financial security in their later years. Here is an example that illustrate the consequences of ignoring retirement planning:

– Mr. N’s Insufficient Savings: Mr. N, in his 30s, neglects retirement planning as he believes he has plenty of time to start saving. He focuses on immediate expenses and desires rather than considering long-term financial goals. As a result, when Mr. N would reach in his late 40s with minimal retirement savings, he will realize that he will have to work longer than anticipated or face a lower standard of living in retirement.

6. Failing to diversify investments:

Putting all your eggs in one basket is risky. Diversify your investments across different asset classes, such as stocks, bonds, and real estate, to reduce risk and potentially increase returns. Failing to diversify investments can expose individuals to unnecessary risk and limit potential returns. Here are a few examples that illustrate the consequences of failing to diversify investments:

– Mr. S’s Concentrated Stock Portfolio: Mr. S works for a single company and has a significant portion of his investment portfolio in company stock. He fails to diversify his investments across different asset classes or industries. If the company experiences financial difficulties or the stock price declines, Mr. S’s entire investment portfolio is at risk, potentially resulting in substantial losses.

7. Overlooking insurance needs:

Adequate insurance coverage is essential to protect yourself and your assets. Review your insurance policies regularly to ensure they align with your needs and circumstances. Overlooking insurance needs can leave individuals vulnerable to financial hardships and unexpected expenses. Here are a few examples that illustrate the consequences of overlooking insurance needs:

– Mr. H’s Lack of Health Insurance: Mr. H decides to forgo health insurance coverage because he believes that he is young and healthy and doesn’t anticipate needing medical care. However, he experiences a sudden illness or injury that requires hospitalization and extensive medical treatments. Without health insurance, Mr. H is burdened with exorbitant medical bills, potentially leading to financial strain and difficulty accessing necessary healthcare services.

– Mr. T’s Neglect of Life Insurance: Mr. T, the primary breadwinner of his family, fails to obtain life insurance coverage. Tragically, he passes away unexpectedly, leaving his family without a financial safety net. His spouse and children are left struggling to cover everyday expenses, mortgage payments, and education costs, as they face financial insecurity due to the lack of life insurance protection.

8. Not regularly reviewing and adjusting your financial plan:

Life circumstances change, and so should your financial plan. Periodically review your plan and make adjustments as needed to stay on track towards your goals.

9. Impulsive spending and lack of savings discipline:

Avoid unnecessary or impulsive purchases that can derail your financial progress. Cultivate disciplined saving habits and practice mindful spending. Impulsive spending and a lack of savings discipline can have detrimental effects on an individual’s financial well-being. Here is an example that illustrate the consequences of impulsive spending and a lack of savings discipline:

– Mr. M’s Inability to Reach Financial Milestones: Mr. M lacks savings discipline and fails to allocate a portion of his income towards savings or investments. He spends impulsively, indulging in luxury items and experiences without considering the impact on his long-term financial goals. As a result, he struggles to accumulate enough savings for major milestones such as buying a home, starting a business, or saving for retirement, hindering his financial progress.

10. Neglecting professional advice:

Consider seeking guidance from financial professionals such as financial advisors or planners. They can provide expertise and help tailor a financial plan to your specific needs. Neglecting professional advice can hinder individuals from making informed financial decisions and maximizing their financial potential. Here are a few fictional examples that illustrate the consequences of neglecting professional advice:

– Mr. F’s Limited Financial Growth: Mr. F dismisses the value of professional financial advice, believing he can handle his financial decisions on his own. However, without expert guidance, he may miss out on strategies for wealth accumulation, tax optimization, or risk management. Mr F’s financial growth potential may be limited, and he may struggle to make optimal decisions that align with her long-term financial goals.

– Mr. J’s Improper Insurance Coverage: Mr. J overlooks the importance of professional advice when selecting insurance policies. He may underestimate the risks he needs to protect against or lack a clear understanding of policy terms and coverage limitations. As a result, Mr. J may have inadequate insurance coverage, leaving him vulnerable to financial losses in the event of unforeseen circumstances such as accidents, natural disasters, or health issues.

As we conclude our deep dive into the intricacies of financial planning, it’s evident that avoiding missteps is crucial for achieving long-term prosperity and security. Having healthy financial practices like establishing an emergency fund, setting clear financial goals, covering your insurance needs, proper retirement planning, and having an experienced financial guide is essential.

We at RichVik Wealth, always aim to continuously bring in financial awareness among our clients, eliminate their chances of making financial mistakes and help them manage their financial health.

To understand more on the topic as well as to start investments please feel free to contact us: